Budget 2022

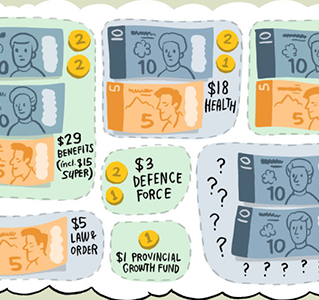

At a time when we need a once in a century Budget to lift us out of our Covid recession, the Government’s response to stimulating growth and investing in critical areas under stress has never been more important.