-

Compliance and audit reviews

From mandates, best practice procedures or accreditations, to simply gaining peace of mind, our technical and industry experts have you covered.

-

External audit

Strengthen business and stakeholder confidence with professionally verified results and insights.

-

Financial reporting advisory

Deep expertise to help you navigate New Zealand’s constantly evolving regulatory environment.

-

Corporate tax

Identify tax issues, risks and opportunities in your organisation, and implement strategies to improve your bottom line.

-

Indirect tax

Stay on top of the indirect taxes that can impact your business at any given time.

-

Individual tax

Preparing today to help you invest in tomorrow.

-

Private business tax structuring

Find the best tax structure for your business.

-

Tax disputes

In a dispute with Inland Revenue or facing an audit? Don’t go it alone.

-

Research & development

R&D tax incentives are often underused and misunderstood – is your business maximising opportunities for making claims?

-

Management reporting

You’re doing well, but could you be doing even better? Discover the power of management reporting.

-

Financial reporting advisory

Deep expertise to help you navigate New Zealand’s constantly evolving regulatory environment.

-

Succession planning

When it comes to a business strategy that’s as important as succession planning, you can’t afford to leave things to chance.

-

Trust management

Fresh perspectives, practical solutions and flexible support for trusts and estate planning.

-

Forecasting and budgeting

Prepare for every likely situation with robust budgeting and forecasting models.

-

Outsourced accounting services

An extension of your team when you need us, so you can focus your time, energy and passion on your business.

-

Setting up in New Zealand

Looking to set up a business in New Zealand? You’ve come to the right place.

-

Policy reviews & development

Turn your risks into strengths with tailored policies that protect, guide and empower your business.

-

Performance improvement

Every business has untapped potential. Unlock yours.

-

Programme & project management

Successfully execute mission-critical changes to your organisation.

-

Strategy

Make a choice about your vision and purpose, where you will play and how you will win – now and into the future.

-

Risk

Manage risks with confidence to support your strategy.

-

Cloud services

Leverage the cloud to keep your data safe, operate more efficiently, reduce costs and create a better experience for your employees and clients.

-

Data analytics

Use your data to make better business decisions.

-

IT assurance

Are your IT systems reliable, safe and compliant?

-

Cyber resilience

As the benefits technology can deliver to your business increases, so too do the opportunities for cybercriminals.

-

Virtual asset advisory

Helping you navigate the world of virtual currencies and decentralised financial systems.

-

Virtual CSO

Security leadership and expertise when you need it.

-

Debt advisory

Raise, refinance, restructure or manage debt to achieve the optimal funding structure for your organisation.

-

Financial modelling

Understand the impact of your decisions before you make them.

-

Raising finance

Access the best source of funding for your business with a sound business strategy and rigorous planning.

-

Business valuations

Valuable decisions require valued insights.

-

Complex and international services

Navigate the complexities of multi-jurisdictional insolvencies.

-

Corporate insolvency

Achieve fair and orderly outcomes if your business – or part of it - is facing insolvency.

-

Independent business review

Is your business viable today? Will it be viable tomorrow? Give your business a health check to find out.

-

Litigation support

Straight forward advice from trusted advisors to support litigation and arbitration matters, expert determinations and other specialist hearings.

-

Business valuations

Valuable decisions require valued insights.

-

Forensic accounting & dispute advisory

Understand the true values, numbers and dollars at stake, as well as your obligations and rights to ensure value is preserved and complexities are managed.

-

Expert witness

Our expert witnesses analyse, interpret, summarise and present complex financial and business-related issues which are understandable and properly supported.

-

Investigation services

A fast and customised response when misconduct occurs in your business.

MBIE options paper about the conduct of financial institutions released

17 May 2019The Ministry of Business, Innovation and Employment (MBIE) recently released a paper for public consultation which includes various options for improving the conduct of financial institutions in New Zealand. The key focus of the paper is to ensure that conduct and culture in the financial sector is delivering good outcomes for all customers. Those wanting to make a submission will need to act quickly as submissions close on 7 June 2019.

Which financial institutions are included in the scope?

MBIE primarily refers to financial institutions in the discussion paper as banks and insurers (including both life and general insurers) to highlight whether the future proposed regime should also scope in other types of financial institutions such as KiwiSaver providers, non-bank deposit takers and lenders. All providers of financial services should take an interest in understanding how financial regulation may develop.

Why is regulation of our financial institutions being considered?

MBIE has identified several reasons for regulation in the financial sector because:

- Financial institutions have a big impact on individuals and the whole economy

- There tends to be an inherent imbalance of knowledge and power between financial institutions and consumers similar to those identified by the Australian Royal Commission into misconduct in the banking, superannuation and financial services industries

- Certain weaknesses were identified by the FMA and RBNZ’s conduct and culture reviews into both banks and life insurers in terms of their governance and management

- Non-regulatory options are insufficient to ensure good conduct.

Problems at the product design stage

- Products are not always designed with good customer outcomes in mind, this was identified by the FMA and RBNZ’s review of life insurer conduct and culture

- Poor value products or products that are not fit-for-purpose; for example, Consumer NZ identified credit card repayment insurance as a product that often provides consumers with very little benefit

- Complexity of financial products can limit a customer’s understanding of what they are purchasing

Problems at the product distribution stage

- Sales are frequently prioritised over good customer outcomes, and there are significant gaps in the measurement and reporting of customer outcomes

- Conflicted remuneration encourages the mis-selling of financial products and services

- There is a lack of oversight of intermediaries

Problems during product use and ongoing interactions

- There is little post-sale follow up of customer outcomes; consumers ‘set and forget’ their financial products, and systems are not always updated to implement new products/promotions

- Insurers have an incentive to underpay claims and sometimes use questionable tactics to settle claims; there are also communication breakdowns when claims take long periods of time or are disputed.

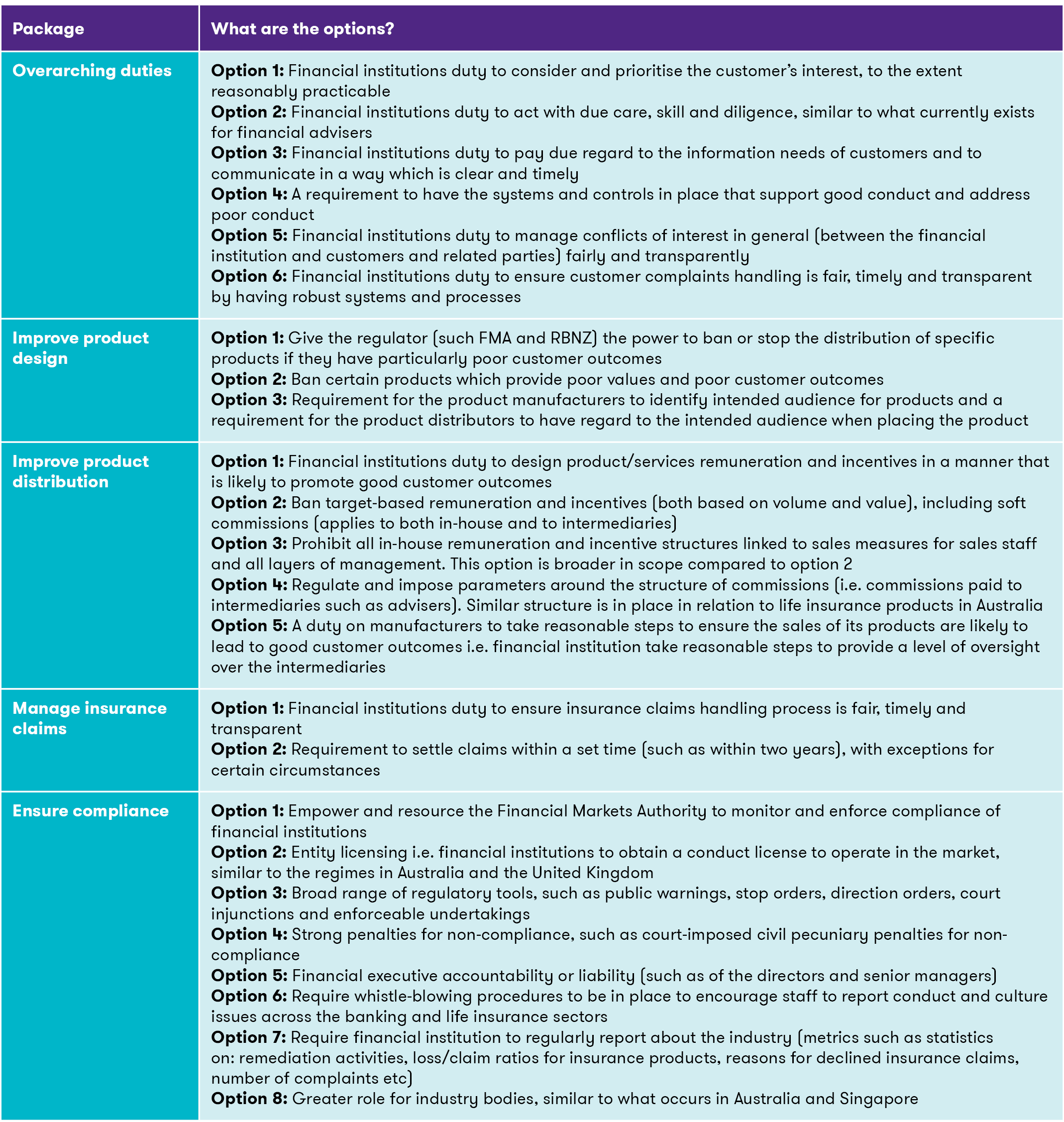

What are the proposed options?

MBIE set out a wide range of options to respond to these matters in its discussion paper. They include suggestions that address both overall and specific obligations (ie, product design, product distribution and insurance claims handling) as noted in the table below:

What is Grant Thornton's view?

New Zealand market participants will already have some experience in aligning their systems and processes to comply with the new regulations. In recent years, New Zealand implemented the AML/CFT Act 2009, the Insurance (Prudential Supervision) Act 2010, the Non-Bank Deposit Takers Act 2013, the Financial Reporting Act 2013, the Financial Markets Conduct Act 2013, and most recently the Financial Services Legislation Amendment Act 2019. There have also been some significant changes in financial reporting standards, including NZ IFRS 9 Financial Instruments and NZ IFRS 17 Insurance Contracts which both require financial institutions to provide transparent reporting, but implementing these comes with additional compliance costs.

Grant Thornton’s view is that that MBIE’s proposed regulation will provide better outcomes for consumers, however, any changes should be scalable. There are some key considerations that financial institutions may need to address when providing their submissions:

- What are the potential compliance costs across different options?

- What changes will be required in the underlying systems to enable compliance with the proposed legislation?

- Can the current training environment deliver the awareness and necessary skills (including the requirements to become a qualified financial adviser) to fully comply with the proposed changes?

- Will the compliance costs impact what consumers pay for products and services?

- Will retaining good talent be impacted if remuneration and incentives need to be modified?

- Would banning products or regulating the production result in a lack of competition in the market?

When is the submission deadline?

MBIE is seeking written submissions on the option paper by 7 June 2019. Following that, submissions will be reviewed, and recommendations will be made to the Minister of Commerce and Consumer Affairs with a view to introduce legislation to Parliament by the end of 2019.

Please note that MBIE is seeking feedback on the drawbacks and benefits of the options identified in the discussion paper, and the overall preferred package, to inform their recommendations to the Minister.

Our view is that this is an important opportunity for all affected financial institutions to contribute to policy formation; Grant Thornton would we pleased to assist you in helping draft a submission for MBIE.

If you have any questions in relation to the Options Paper, making a submission, or are considering how these changes affect you or your business, please contact us.