Mandatory climate related reporting on the way for some NZ businesses

David Pacey

20 Oct 2021

David Pacey

20 Oct 2021

The Government is establishing a standardised approach to climate-related reporting for certain entities to disclose their progress on emission reduction in a way that’s transparent and consistent. It has introduced an amendment to the Financial Markets Conduct Act (2013) to make climate-related reporting mandatory for many New Zealand organisations. These requirements come into effect from 1 January 2023, and an initial partial draft of the proposed standard was released for public comment on 20 October 2021.

Why now?

Climate change is a clear and present danger to businesses everywhere, and this poses a major risk to the stability of financial systems globally. For example, your business might experience supply chain disruptions due to adverse weather events, or your consumers’ buying behaviour might change as their preferences shift to more sustainable, environmentally friendly products and services. And there’s the increasing cost of obtaining insurance for climate risks to consider as well.

Therefore, the pressure on organisations to be more transparent about their exposure to climate-related financial risk is increasing. New Zealand businesses currently provide little or no information about the implications of this risk, and where disclosures are actually made, the outputs and reports are often delivered inconsistently; this reduces transparency for investors and makes accurate reporting about the country’s progress towards a zero-carbon future difficult.

In addition to greater transparency, standardised climate related financial disclosure is also expected to enable climate risk to be adequately priced in capital markets and help the Government achieve its zero-carbon target by 2050.

Who is impacted?

Mandatory reporting: regulated institutions

It's expected that the following types of entities will be mandated to report on their levels of climate related risk:

- Registered banks, credit unions, and building societies with total assets of more than $1 billion

- Managers of registered investment schemes with more than $1 billion under management

- Licensed insurers with more than $1 billion total assets under management, or annual premium income greater than $250 million

- Equity and debt issuers listed on the NZX with a market capitalisation greater than $60 million

- Crown financial institutions with more than $1 billion total assets under management

Non-mandatory reporting: Forward-thinking businesses

Privately owned businesses and other organisations are currently exempt from the proposed disclosure requirements. However, having a consistent method of reporting climate related risk against emission reduction targets is a compelling value proposition for forward-thinking entities to jump on board. There is an increasing demand from suppliers, employees and customers for businesses to be transparent about how they are managing their impact on the climate. Reporting your business’s impact on the environment against a robust framework will create a competitive edge and positive engagement with your brand.

What reporting will be required?

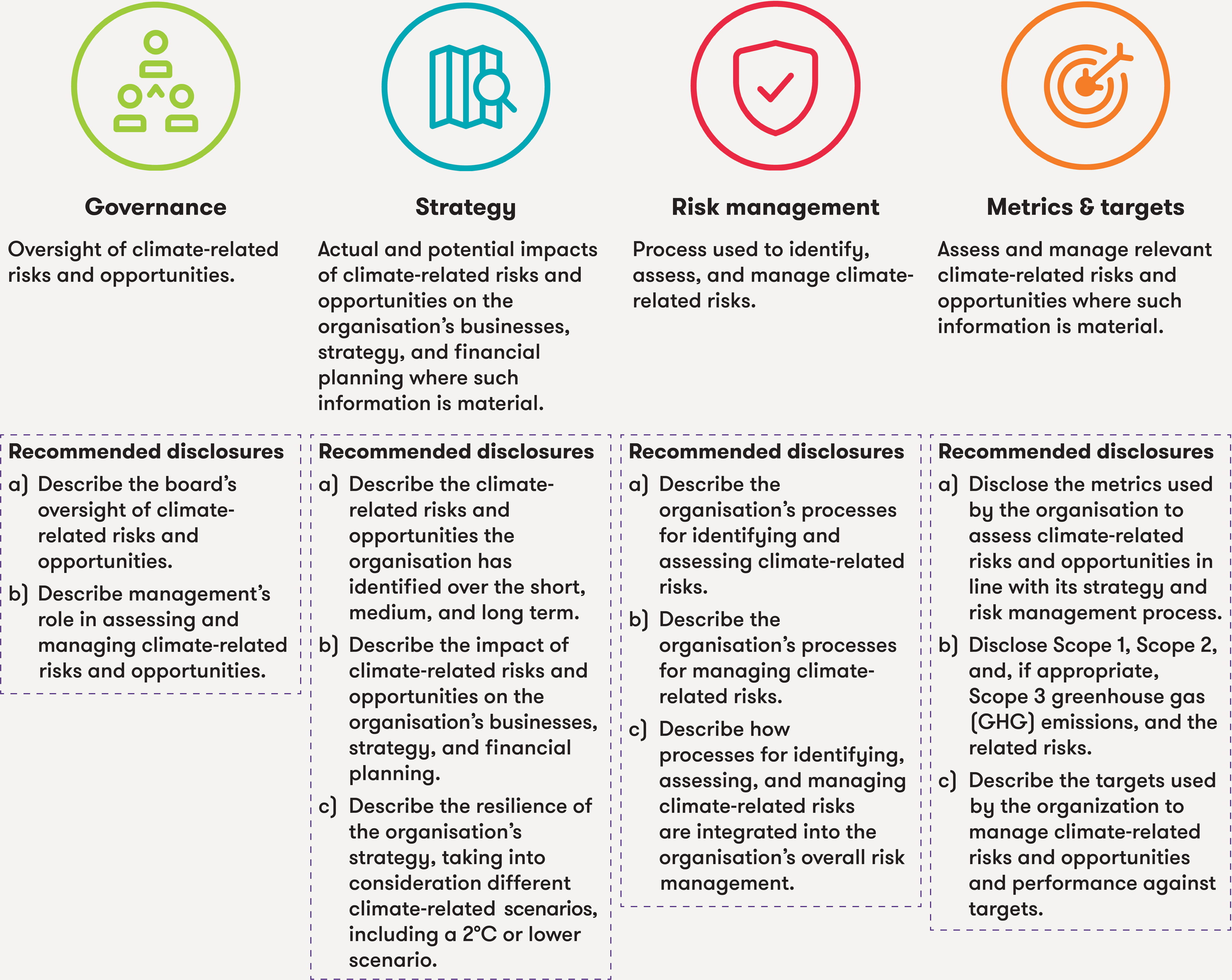

The External Reporting Board (XRB) is tasked with developing the standard for climate-related disclosures. The standards are being developed in line with the Task Force on Climate Change-related Financial Disclosures (TCFD) recommendations. The standard will also require organisations to assess the risks and opportunities of climate to their business across four themes:

When will mandatory reporting take effect?

While this new legislation still needs to be approved by Parliament, impacted organisations will be required to make disclosures for reporting periods beginning on or after 1 January 2023. We understand comparatives will not be required in the first year.

The XRB has provided the following timetable for the development of its climate related standard:

|

20 October 2021 Governance and risk management |

March 2022 Strategy, and metrics and targets |

July 2022 Formal exposure draft |

| This initial draft will be released for a 4-week consultation period, closing Monday 22 November 2021. | This initial draft will seek feedback on implementation feasibility. It will also include specific discussion about the topics of scenario analysis and GHG accounting. The draft will be released for a 4-week consultation period. | This formal exposure draft will include accompanying documents, such as transitional provisions, and will be released for a 3-month consultation period. |

Next steps

You can now have your say about the proposed disclosure regime. Submissions for the first phase close on 22 November 2021.

At Grant Thornton we have a range of professionals dedicated to assist you through this journey. We can help your organisation formulate a request for feedback on the consultation documents, complete a gap analysis of your current climate reporting, or discuss assurance options regarding the proposed disclosures. Whatever the next steps are for your organisation, the time to start the process is now as mandatory reporting starts in just over a year.