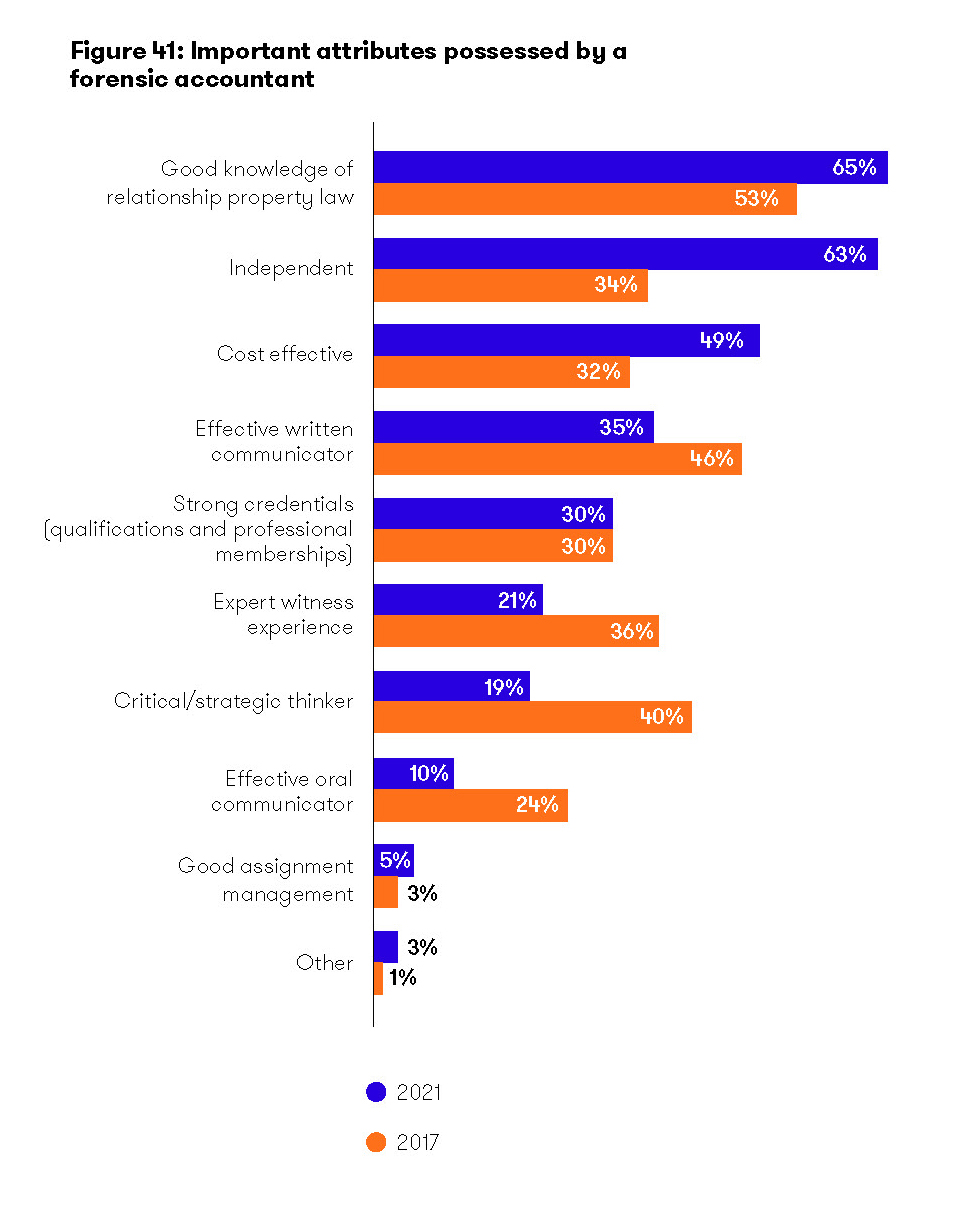

What are the professional attributes that relationship property lawyers look for most in their forensic accountant? The latest New Zealand Relationship Property Survey by Grant Thornton and the New Zealand Law Society asked practitioners to list the three most important attributes a forensic accountant should have in giving expert advice in relationship property matters. The findings contain valuable insights for practitioners and experts alike.

The survey findings show forensic accountants (including business valuers) regularly, and increasingly, form part of the team that relationship property lawyers assemble to advise their clients. In the last two years, nearly half (46%) of practitioners had instructed a forensic accountant, up from 42% in 2017.This finding also highlights the team approach many practitioners now take to best advise their clients on relationship property matters.

In that period the most common instructions were for share and business valuations and s15 (economic disparity) calculations, with 94% and 60%, respectively, having given instructions. New Zealand’s economy is characterised by many owner-operated businesses, so it is unsurprising business and share valuations were easily the most common instruction.

Of those lawyers who had instructed a forensic accountant, 65% said that the most important attribute was a good knowledge of relationship property law, which underlines the technical nature of this area. We take this to mean that lawyers want their accountant’s focus to remain on the “numbers”, but numbers that are soundly based on the appropriate legal principles and precedent.

This finding appears consistent with a substantial increase in the use of forensic accountants for the calculation of s15 (economic disparity) claims, one of the more technical and precedent based areas.

The lawyers surveyed also stressed the importance of an independent forensic accountant, with 63% putting this in their top three. This finding strongly suggests most relationship property lawyers are not interested in a “hired gun” but an expert who will consider the issues on their merits and is cognisant of their overriding duty to assist the court impartially on matters within their expertise.

The requirement for independence is also consistent with another survey finding: a significant 11% increase in lawyers who had used a single joint forensic accountant in the last two years. In 2017 only 27% of practitioners had used this approach, jumping to 38% in 2021.

Cost effectiveness was also identified as an important attribute for forensic accountants, again a substantial increase from the 2017 survey results. The 2021 survey covered the first two years of the pandemic, so this might be attributable to budget restraints imposed by Covid-19. It is also important to note cost effectiveness implies value for money and is not the same as lowest cost.

Finally, it is interesting to observe a marked decrease in those practitioners who require their forensic accountant to have expert witness experience. While 36% put this in their top three attributes in 2017, this has now decreased to 21% of practitioners. This may reflect lawyers becoming increasingly comfortable this experience is unlikely to be needed given relationship property cases usually settle out of court. It may also reflect the limited number of forensic accountants in New Zealand with experience of giving expert evidence in court.